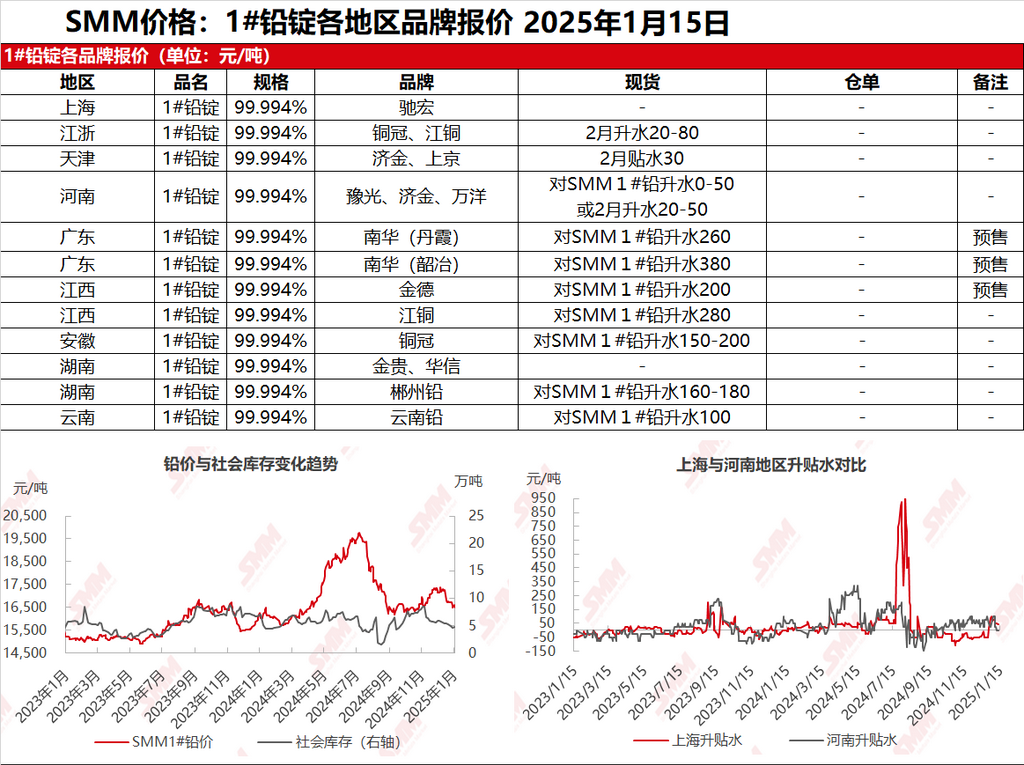

SMM, January 15: Quotations were scarce in the Shanghai market; in Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 16,590-16,680 yuan/mt, with a premium of 20-80 yuan/mt against the SHFE lead 2502 contract. SHFE lead moved downwards after a higher opening, and suppliers shipped goods following market trends. As today was the delivery date, warehouse warrant cargo quotations were limited, with shipments mainly consisting of cargoes self-picked up from production sites. Some suppliers continued to lower premiums for shipments. During this period, secondary lead smelters were also actively shipping, with some reducing premiums. Secondary refined lead was quoted at a premium of 0-50 yuan/mt ex-factory against the SMM 1# lead average price, while transactions at a premium of around 100 yuan/mt were difficult. Downstream enterprises gradually completed pre-holiday stockpiling, and spot trading activity slowed down.

In other markets: The SMM 1# lead price rose by 100 yuan/mt compared to the previous trading day. In Henan, pre-sales and long-term contract cargo pick-up remained dominant, with some suppliers standing firm on quotes and reluctant to sell. In Hunan, premiums remained at 150-200 yuan/mt, with downstream maintaining just-in-time procurement. Meanwhile, in Jiangxi, Yunnan, Guangdong, and other regions, primary lead supply had not resumed, and quotations remained firm. Pre-holiday just-in-time stockpiling by downstream enterprises was nearing completion, and transactions gradually slowed down.

![SHFE Lead Prices Lacked Upward Momentum, and the Pattern of Doldrums Was Difficult to Change [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![LME Lead Rebounded Strongly After Hitting Bottom; SHFE Lead Opened Higher With a Gap, Came Under Pressure, and Pulled Back [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)